The 16th edition of the forum will take place in Paris on March 20-21, 2023, with a key focus on the theme of Finance & Society. We invite you to submit research papers electronically in PDF format

“FAIRE FACE AUX NOUVEAUX DÉFIS” – 34ème CIMEF

34ème Concours International des Mémoires de l’Économie et de la Finance – Deadline 31.12.2022

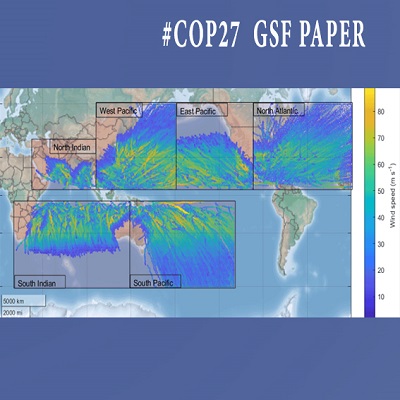

#COP27 ‘Cyclone Generation Algorithm for National Damage Assessment’

GSF Paper published in the Geoscientific Model Development Journal, co-authored by Peter Tankov, Théo Le Guenedal and Philippe Drobinski

Estimating dynamic systemic risk measures

CREST Working Papers Series No. 2022-11

by Loïc Cantin, Christian Francq and Jean-Michel Zakoïan

Inference on Multiplicative Component GARCH without any Small-Order Moment

CREST Working Papers Series No. 2022-09

by Christian Francq, Baye Matar Kandji and Jean-Michel Zakoian

Local Asymptotic Normality of General Conditionally Heteroskedastic and Score-Driven Time-Series Models

CREST Working Papers Series No. 2022-06

by Christian Francq and Jean-Michel Zakoïan

Iterated Function Systems driven by non independent sequences: structure and inference

CREST Working Papers Series No. 2022-03

Forecasting Financial Markets with Semantic Network Analysis in the COVID—19 Crisis

CREST Working Papers Series No. 2021-06

by Andrea Fronzetti Colladon, Stefano Grassi, Francesco Ravazollo and Francesco Violante